Philhealth to increase contribution rate to 3.5% in 2021

Philhealth contribution rate in 2021 is at 3.5%.

-

Philhealth will increase members’ contribution rate to 3.5% effective January 2021.

-

The increase is pursuant to the Universal Health Care Act, to fund the numerous reforms under the law.

Once again, Philhealth will increase the contribution rate of direct contributors starting in January 2021. Check the Philhealth contribution table 2021 in this post.

PhilHealth President and CEO Atty. Dante Gierran said in a press statement that the rate hike will push through as mandated by Universal Health Care (UHC) Law.

“PhilHealth fully recognizes the current pandemic situation that is taking its toll on many businesses and livelihood of many Filipinos. However, it is bound to implement the UHC Law which has been the beacon and source of hope for the country that is aiming for better healthcare services even as it battles the Coronavirus Disease 2019,” Gierran said.

The increase in premium contributions will ensure sufficient funding for the health care benefits of its 110 million members, he added.

The premium adjustment is provided for in Section 10 of the UHC Law and its implementing rules and regulations, the guidelines of which are contained in Circular 2020-005 published by PhiiHealth on March 5, 2020. The implementation started November 2019 when the rate was increased to 2.75%, then 3% in 2020.

It will continue its annual increase of 0.5 percentage point until it reaches 5% by 2025.

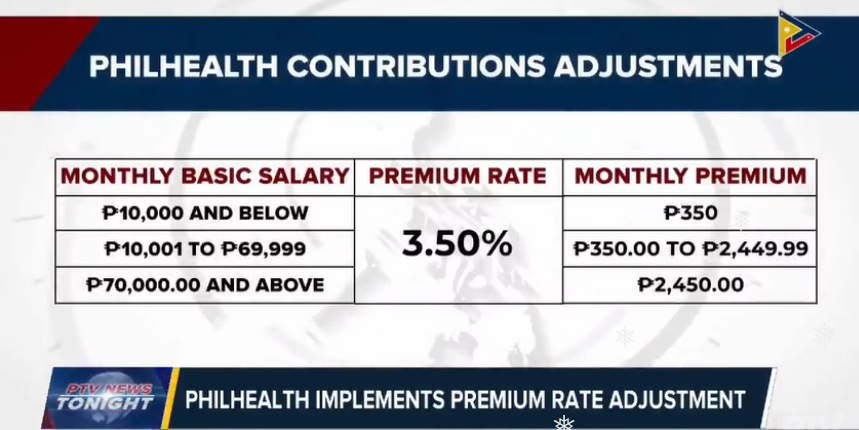

Philhealth Contribution Table 2021 for Direct Contributors

Member Contributions of Direct Contributors starting in January 2021 are as follows:

Those earning below P10,000 shall be fixed at P350/month while those earning P70,000/month or higher is fixed at P2,450/month. Contributions of employed members (including Kasambahays) shall be equally shared between employees and employers, while those of self-paying members, professional practitioners and land-based migrant workers, and other direct contributors with no employee employer relationship are computed straight based on their monthly earnings and paid wholly by the member.

The law emphasized the importance of members’ social health insurance contributions to provide the necessary funding for various reforms under the UHC that are now being availed of by Filipinos such as but not limited to the following:

1. Automatic membership of all Filipinos into the National Health Insurance Program, ensuring access to quality healthcare as a fundamental right and not for the privileged few.

2. Immediate eligibility of all Filipinos to PhilHealth benefits each time they seek treatment at and confinement in any accredited hospitals in the country and even overseas.This means that the former sufficient eligibility rules and contribution requirements are no longer applicable.

3. Assignment of every Filipino to a primary care provider (or PCP) of their choice initially in pilot areas to be identified in each region in 2021. Accreditation of PCPs shall commence immediately. This program is called Konsulta or Konsultasyong Sulit at Tama.

The PCPs under Konsulta will act as patients’ navigator, coordinator and their initial and continuing point of contact through the health care delivery system. The PCPs will also be responsible for the health and well-being of patients assigned under their care, and are expected to detect and help arrest diseases at the early stages in order to prevent costly treatments later on.

It is also envisioned that PhilHealth will be covering more catastrophic illnesses as soon as additional funding is made available, as stipulated in the UHC Law.

4. No co-payment (or No Balance Billing) for confinements in basic or ward accommodations in both government and private healthcare facilities, except when availing of amenities, for which PhiiHealth will develop co-payment limits to make costs predictable. The legislated contribution scheme will enable patients to enjoy substantial financial risk protection through the gradual decrease in out-of-pocket expenses.

5. Lifetime PhilHealth coverage for all members upon reaching the age of retirement and after contributing at least 120 months to the Program, ensuring continuing financial protection from health risks brought about by old age.

“These reforms and those that are still in the pipeline as mandated by the UHC Law are for the benefit of all and sundry, regardless of their station in life. Everyone’s hard-earned contribution will help guarantee that all these gains are delivered and sustained for all Filipinos today, tomorrow and for the years to come,” Gierran said.